Understanding the difference between a payment gateway and a payment processor is vital for any business that accepts online or card-based payments. Confusing these two can lead to poor choices in infrastructure, which may affect security, compliance, and how quickly you receive funds. A clear grasp of their distinct roles helps businesses build reliable, efficient payment flows and choose the right partners or solutions.

What a Payment Gateway Is and What It Does

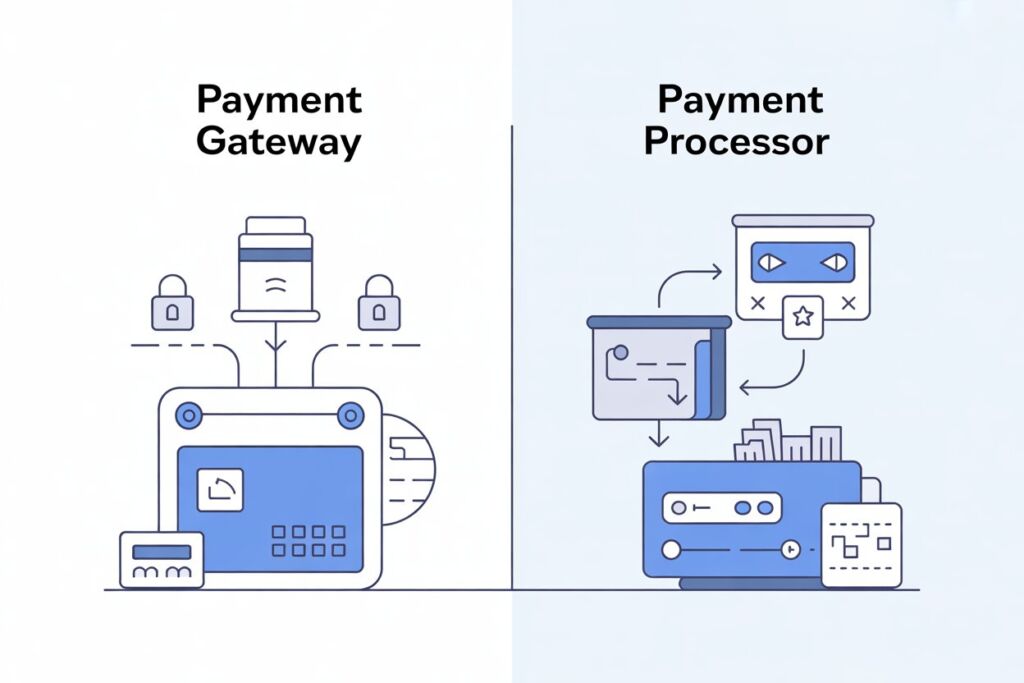

A payment gateway is a software layer, either embedded in a website or provided by a third-party service, that collects a customer’s payment information at checkout. When a buyer enters their credit or debit card number, expiration date, CVV, or other payment details, the gateway captures that information. It then securely encrypts and/or tokenizes the data to protect it before transmitting it to a payment processor or acquiring bank. The gateway does not itself move money. Instead, it acts as a secure conduit between the merchant’s frontend (website or app) and the backend payment infrastructure. Typical responsibilities may include: collecting card or payment data; encrypting or tokenizing sensitive details; verifying CVV or billing address; enabling support for different payment methods (credit/debit cards, digital wallets, bank transfers); and offering various integration options such as redirect flows, iframe embeds, plugins, or APIs. To better understand the security standards that gateways must follow, businesses frequently refer to the official PCI DSS guidelines.

What a Payment Processor Is and How It Works Behind the Scenes

A payment processor is the service or system that actually handles the transaction behind the scenes. Once a payment gateway passes along the encrypted payment data, the processor takes over. It communicates with the card networks, the customer’s issuing bank, and the merchant’s acquiring bank to authorize and facilitate the transfer of funds. The payment processor verifies that the card is valid and that the customer has sufficient funds, then requests authorization from the issuing bank. If approved, the processor schedules settlement: the funds are moved from the customer’s account through the card network to the acquiring bank and eventually credited to the merchant’s account. Some processors provide additional services around fraud detection, refund handling, chargeback management, reporting, and compliance. A clear and visual explanation of how processors interact with the card networks can be found in the official Visa payment processing overview.

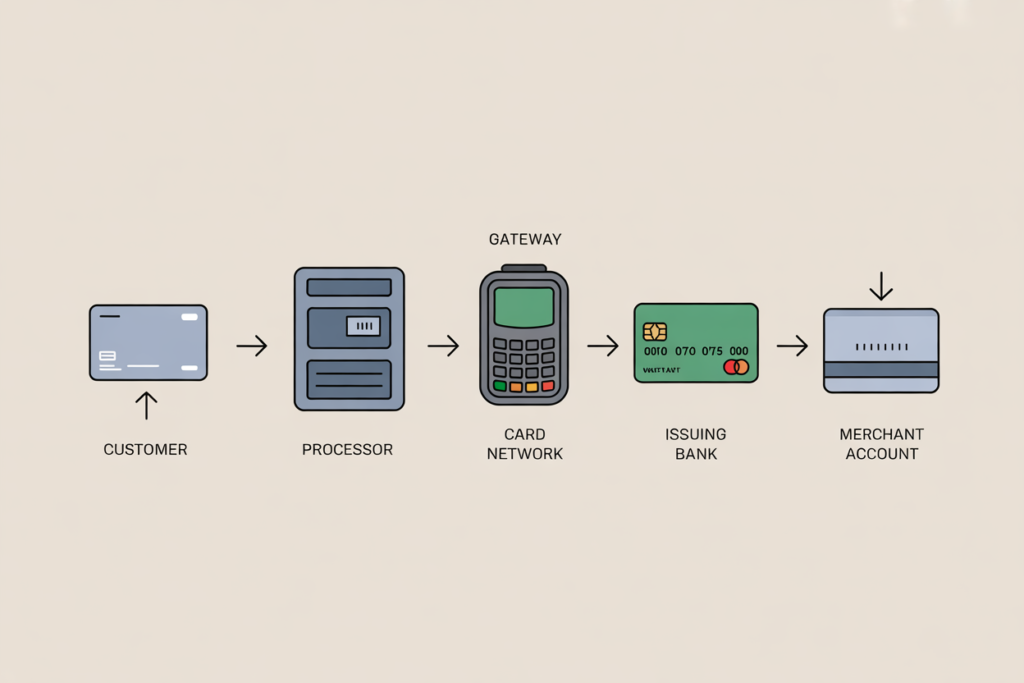

How a Transaction Flows With Gateway and Processor

Typical online payment steps:

- The customer enters their card or payment details on the merchant’s website or app via the payment gateway form.

- The gateway encrypts (or tokenizes) the payment data and sends it securely to the payment processor.

- The processor forwards the data to the card network or issuing bank to check validity and funds availability. That bank either approves or declines the request.

- The processor sends the response back to the gateway. The gateway communicates the result to the merchant’s frontend.

- If approved, the processor initiates fund transfer: settlement occurs, and funds are transmitted from the issuing bank to the acquiring bank, then to the merchant’s account.

Authorization usually happens within seconds. Settlement, the actual movement of funds, may take from the same day up to several days depending on banks and processors.

Key Functional Differences Between Gateway and Processor

This comparison table summarizes how payment gateways and payment processors differ in their core role, where they sit in the payment chain, whether they handle the actual flow of funds, and which extra services they typically provide. Reviewing these points helps you understand which type of provider is the best operational fit for your business.

| Function / Role | Payment Gateway | Payment Processor |

|---|---|---|

| Primary job | Collects and securely transmits payment data | Processes transaction, authorizes and settles payment |

| Position in payment chain | Frontend, connected to website or app checkout | Backend, interacts with card networks and banks |

| Money flow | Does not move funds | Moves funds from customer to merchant |

| Requirement of merchant account | Usually requires merchant account to settle funds | Linked to merchant account and acquiring bank |

| Extra services | May provide basic fraud checks, encryption, tokenization | Can offer fraud detection, chargeback management, settlement, reporting |

Why Some Businesses Use Separate Gateway and Processor While Others Use Unified Solutions

There are providers that only offer gateways, only processors, or both together as a bundled solution. Using separate components can give businesses flexibility. For instance, you might prefer a specialized gateway for advanced checkout customization but pair it with a processor that offers better settlement terms or fraud tools. A helpful resource for comparing gateway types is the guide from bilixe. For many merchants, especially small or online businesses, unified solutions that combine gateway, processing, and merchant account services simplify setup and reduce operational complexity. A well-known provider doing this is Stripe. Businesses also browse directories like the payment providers catalog on bilixe when researching suitable platforms. If a business has high volume or needs specific bank relationships, separating gateway and processor might make sense. But for most standard e-commerce or service-based businesses, an all-in-one approach offers convenience.

When Gateways and Processors Are Typically Used

Online stores, mobile apps, and any “card not present” contexts rely on payment gateways to collect payment information and send it for processing. Websites, e-commerce platforms, and digital services commonly integrate a gateway. Payment processors are needed whenever money moves, regardless of method. That includes online transactions via a gateway, in-store purchases using POS terminals or card readers, bank transfers, digital wallets, and other payment methods supported by the processor.

Security, Compliance and Risk Responsibilities

The payment gateway plays a crucial role in protecting customer payment data. By encrypting or tokenizing card information and offloading sensitive data from a merchant’s systems, a gateway reduces the merchant’s burden under security standards such as PCI DSS. Many gateways also offer basic fraud checks like CVV verification or address validation. The payment processor handles deeper aspects of risk management and compliance. It interacts with banks and card networks to verify card legitimacy, check for fraud, manage chargebacks or disputes, and ensure settlement follows banking regulations. This separation of duties helps maintain data security and regulatory compliance while minimizing the scope of sensitive data exposure at the merchant’s end.

Examples of Real-World Providers and Solutions

Some services offer only a gateway, others only processing, and many provide both. For instance, Stripe bundles gateway, processor, and merchant account functionality into one integrated offering. Businesses researching such solutions often explore platforms like bilixe for structured comparisons. Other providers may specialize. A standalone gateway might link with a third-party processor chosen by the merchant, or a processor may integrate with a custom gateway or POS system to support in-store payments. This modular approach gives businesses flexibility to mix and match services based on their payment needs.

Which Approach Works Best Depends on Your Business Needs

Choosing between a separate gateway and processor or a unified solution depends on factors like your sales channels, payment volume, and technical or compliance requirements. For purely online, small-to-medium merchants, integrated solutions are often the easiest and most cost-effective way to accept payments. For larger, high-volume merchants or those with specialized needs, such as diverse payment methods, global operations, or custom risk and settlement rules, splitting gateway and processing or selecting specialized providers may provide greater control and flexibility.